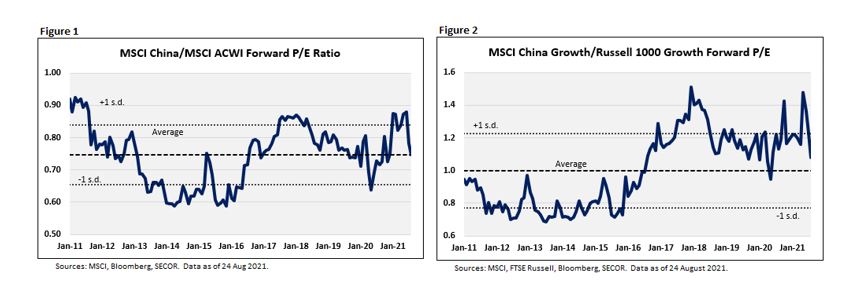

It is worth noting that these valuations are based on analysts’ expected earnings which may not yet fully account for the negative impact on earnings from the recent changes in the operating environment, especially for China’s largest and fastest growing technology companies at the centre of the crackdown.

Other Regulatory Tightening Cycles

Public companies in China have found themselves in the regulatory crosshairs on prior occasions, including a pair of notable instances when its market leaders were targeted. The first such instance targeted Telecommunications companies in 2001. Telecom stocks represented approximately 60% of the MSCI China index weight in the early 2000s, even more than the approximately 50% peak weight today’s Internet sector enjoyed before the most recent clampdown. The second instance, which began in 2011, placed Banks in the regulatory sights. Financial stocks had by then taken up the mantle of index leadership, accounting for roughly 40% off the MSCI China index with four banks ranking among the six largest companies at the time.

The common thread in these instances is that as sectors grew into their dominant position the central government required them to assume greater social responsibility, altering their mission from maximizing shareholder value to serving the real economy.[2] For instance, China’s telecoms were saddled with building one of the world’s most extensive mobile networks, while also cutting fees. Today, these companies have one of the lowest average revenue per user versus global peers along with onerous levels of capital expenditures. Banks were required to make unsound loans to zombie companies that served perceived national interest, resulting in high credit costs and reserve allowances relative to global standards. These once-dominant telecom and financial companies predictably suffered lower margins, decelerating earnings growth, valuation multiple contraction and disappointing returns.

This history of requiring its most successful companies to serve both shareholders and the national interest should not be an insurmountable barrier to attracting capital going forward. China’s massive economy, population and rapid economic growth will continue to provide a strong attraction for capital, despite the hurdles. China has the second largest economy in the world with a GDP of $14.7 trillion, nearly 3 times the size of third place Japan. And although growth over the next several years is expected to moderate to around 5%, such growth is still the envy of the developed world, putting China on a path to surpass the US around 2030. It is populated by 1.4 billion people with rapidly growing disposable incomes. Like in the aftermath of past episodes of regulatory tightening, capital will likely continue to flow to China when this wave has crested because of its unique growth opportunity.

Fuzzy Relationship between GDP Growth & Equity Returns

So why has China’s strong economic growth failed to translate into strong equity market returns? The country does not appear unique in this circumstance. In fact, the intuitive notion that high GDP growth should lead to superior equity returns has been the subject of a body of research that has found a weak or non-existent leak between the two, while others have shown an even more counterintuitive result where countries that have experienced high economic growth have tended to deliver relatively weak equity returns.[3]

There have of course been exceptions to these findings, maybe most notably the case of the US which has provided superior returns along with strong economic growth relative to other developed nations over the trailing decade. But the higher growth emerging market countries, even omitting China, have delivered inferior equity returns with the MSCI Emerging Market ex China index returning 9.3% over the decade ending 20 August 2021 versus 14.5% for the slower growing developed markets captured by the MSCI World index.

Probably the best explanation for the weak link between the economic growth and stock market returns is attributable to differences between the growth of aggregate earnings at the country level that figures in GDP growth and the growth in earnings available to public equity investors that drives equity returns. In countries such as China with a large public sector, stock market industry and sector composition can diverge significantly from the economy at large. While China has opened up to the outside world since the 1990s when it re-opened its stock exchanges, it still remains a relatively closed society in comparison to most of the world and as recent actions have reminded us, protective of key assets that it is reluctant to share with the rest of the world. Additionally, equity returns are influenced by other factors such as interest rates and the multiple that investors assign to the portion of earnings available to them, further muddying the link.

Another related explanation is that globalization has further clouded the link between earnings growth for the economy versus the stock market with many multi-nationals now earning a large share of their total profits outside of the country in which they are domiciled. As a result, parts of the production process for multinationals may not be included in a country’s GDP. This potential decoupling probably does not help explain the poor performance of China’s stocks relative to its GDP though, particularly as China’s stock market has tended to be dominated by companies that have been primarily domestic-focused – first Telecoms, then Financials and most recently Internet-related.

Yet another potential explanation is that investors impound the superior growth outlook for the economy into the prices of the country’s stocks.[3] This argument is similar to that explaining the superior long-term performance of low-expectation value stocks versus their high-expectation counterpart growth stocks. A notable historical example of this is the case of the fast-growing Japanese economy of forty years ago and its subsequent stock market torpor over the following couple of decades where equity returns badly trailed the rate of growth in the economy. China’s explosive economic growth has certainly been no secret and it is possible that high economic growth expectations there have similarly fuelled overly optimistic valuations by its public equity investors. It is worth noting that China has a very large and very active retail investor base not renowned for its long investment horizon. The high expectations of this impatient investor group have likely contributed to the frustrations in converting China’s strong economic growth into equally strong equity returns.

Many Flavours of Capitalism

The Chinese form of capitalism stands in contrast to that in the US where the mission of the corporation is to maximize value for its owners (although this has increasingly been questioned of late). A closer comparison is probably the model employed in much of Europe where corporations are more likely to serve not only shareholders, but also a range of stakeholders, and attempt a delicate balance of the two. While recent equity returns and levels of profitability of the European model have lagged those of the US, notable examples such as Germany, with a long-term track record more comparable to the US in these regards, support the notion that satisfying outcomes can be attained for all constituencies.

The pressure to serve society is even more explicit with China’s state-sponsored capitalism and combining capitalism with an authoritarian regime is certainly concerning to Western eyes that witnessed failures of command economies in the Soviet Union and Cuba. Perhaps the closest analogue of blending capitalistic and social goals is Singapore, albeit in a democratic state. But even here the returns have been disappointing with MSCI Singapore returning 4.4%/year since 1994, despite GDP growth of 5.8%/year over that period. Its return also trails the return of the global ACWI index by 3.3%/year (returns USD) over that period. Striking the balance between serving shareholders and society is also likely an easier task in a city-state of 6 million people rather than an emerging superpower with a 1.4 billion people, making even this analogy a weak one at best and further highlights how unique a case China represents.

Of course, the less restrained model of capitalism in the US has come with its own undesirable side effects, most notably social fairness issues, many of which are now boiling over and forcing much delayed reckonings. Additionally, a more hawkish Biden administration has signalled its intent to curtail the market power of the US tech giants which has the potential to derail their exceptional stock market performance and by extension the entire US equity market given their dominant positions. The two-party system of the US will likely blunt any potential regulatory impacts in comparison to the situation in China where the goals of the Communist Party can be implemented with little resistance. Whether concrete actions ultimately come to pass, it is hard to ignore that after years of a hands-off approach toward business, the regulatory winds appear to be shifting in the US. Should the US shift to its own version of a more inclusive form of capitalism, this could reduce any relative disadvantage China may face in attracting capital.

Opportunities & Challenges

A potential mitigant in the Chinese government potentially deepening or broadening the recent crackdown is the country’s continuing need to attract capital to fuel its economic transformation. Despite huge strides over the past decades, median household income in China is still just $6,200, which is about average globally but well behind the level of countries classified as developed (e.g., US: $43,600, Japan: $33,800).[5] Unleashing the capitalistic spirits of its citizens has been a key driver of the progress that has been made in narrowing gap thereby ensuring its survival, although in a form that will continue to look strange to most Westerners.

With much of the low hanging fruit from economic liberalization, industrialization, favourable demographics, and urbanization having been plucked, the pace of growth will continue to decelerate. Although 5% economic growth would be the envy of most of the world, it is a far cry from the double-digit growth it routinely achieved a decade ago. From its now much larger base, economic growth will inexorably converge with the rest of the world.

Keeping the economic machine humming in coming years will not be without its challenges. As a result of decades of state-enforced fertility limits, China’s population growth has moderated and will soon begin to shrink. A shrinking working age population and a surge in the elderly in coming years will divert resources that could otherwise be aimed at productive investment. Its rapidly growing defence budget will also remain hungry for resources and its extended residential real estate market has potential to become a major headache due to its outsized contribution to economic activity.

As economic gains moderate, improvements in productivity will be needed to reach its 5% growth target. This will require continued innovation in information technology, but the recent crackdown that has made life less rewarding for its richest citizens could send a chill through the next generation of innovators who may not be as motivated by the prospect of sharing much of the benefit of their creations with the state.

In its quest for technological supremacy, China’s government has signalled its intention to focus on the “harder” areas of technology, such as artificial intelligence, robotics, data security, and biotech, and less on the “softer” areas such as social networking and gaming that they view as societal ills. In ignoring these areas, they run the risk of foregoing potential advances that may be transferrable to the very fields they wish to emphasize.

The continued need for capital and the sharp sell-off in its equity markets have triggered some recent damage control on the part of the central government in an effort to reassure investors. Government officials have recently made statements such as China aims to “strike a balance between… social fairness and competition and promote healthy development of the capital market” and the “Common Prosperity initiative does not mean absolutely equal.”[6] Recognizing that they cannot completely alienate potential providers of capital, government actions that demonstrate these words will go a long way toward reassuring sceptical investors.

Conclusion

China’s massive market and remarkable growth story has attracted investors since its stock markets re-opened in 1990, but equity investors have been disappointed by low returns that have failed to match the rapid growth of the underlying economy. The recent crackdown by China’s government has surprised equity investors, evidenced by the recent sharp drop in the nation’s stocks. Given the history of China’s public equity markets, maybe it should not have been so surprising.

The market opportunity remains far too large to ignore and the opportunity set for active equity management should be sizeable as well for the discriminating investor who can successfully evaluate the outsized risks that accompany the outsized opportunity. The economic growth story, if not as compelling as when China re-opened its doors to investors, remains attractive relative to the rest of the world. If the relatively short history of China’s stock markets serves as a guide, this robust economic backdrop coupled with embrace of capitalism by the Chinese people should continue to provide a fertile environment for investors to identify the individual companies that are likely to emerge with the potential to deliver superior performance for shareholders.

However, a history that is also filled with instances of shareholders’ interests being subordinated to social goals in a one-party authoritarian state calls for caution going forward. The optimistic case hinges on the country’s ongoing need to attract capital prompting authorities to balance their social objectives with the need to provide sufficient rewards for shareholders. The country’s track record, however, shows little evidence of striking this difficult balance nor do recent events invite optimism. The potent combination of a fast-growing economy and the prospect of tapping into that growth through its most dynamic public companies will no doubt continue its irresistible pull to equity investors. Will they be able to adequately temper their enthusiasm? And will they be allowed to fully enjoy the benefits typically afforded shareholders around the world? I wouldn’t bet on it.