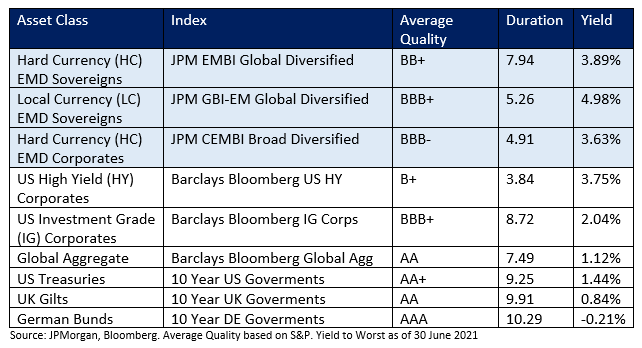

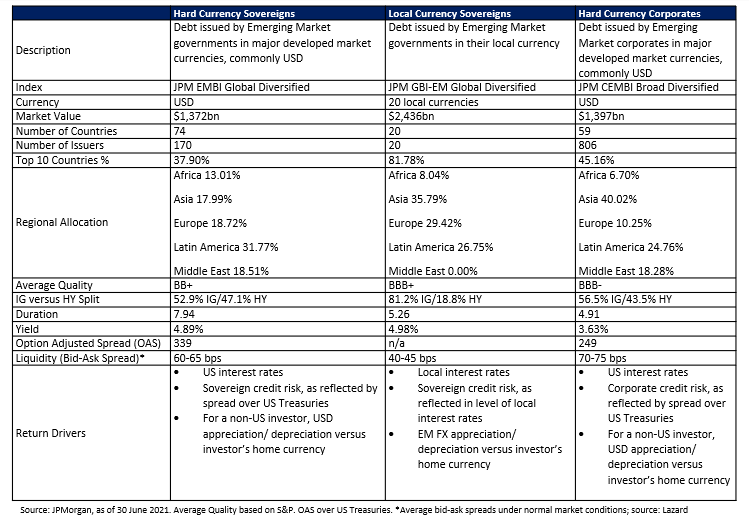

The characteristics detailed in the table above are based on the JPMorgan indices, which is the preferred benchmark for the majority of investment managers we follow. Other index providers, for example Bloomberg Barclays, may have slightly different inclusion rules and additional criteria (such as floors and caps for country weights), but all follow similar benchmark segmentation with regards to splitting the investible universe into Hard Currency Sovereigns, Local Currency Sovereigns, and Hard Currency Corporates.

The three sub-sectors differ on various metrics, which we discuss below.

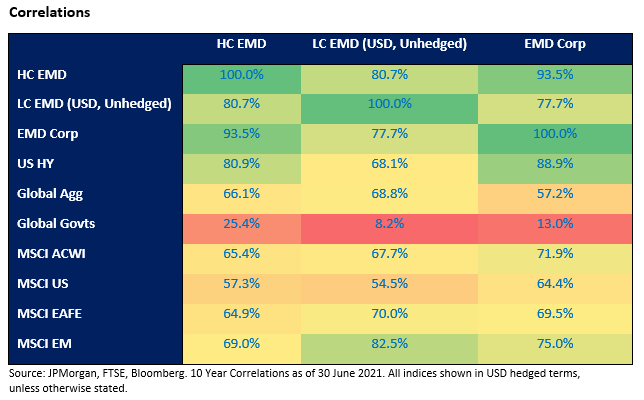

Diversification: The Hard Currency EMD Sovereign index is well diversified by country and by region, with 74 countries well balanced across Africa, Asia, Europe, Latin America, and the Middle East, offering ample opportunities for alpha generation through country selection. The Hard Currency EMD Corporate index is similarly well diversified, with 59 countries and 806 issuers, although over 40% of regional exposure lies in China, and less than 10% in Africa. The Local Currency EMD Sovereign index is relatively less diversified, with only 20 issuers, and over 80% of the index in the top 10 countries.

Duration: The Hard Currency EMD Sovereign index has a duration of 7.94, significantly above that of the Local Currency Sovereign and Hard Currency Corporate indices, which have durations of 5.26 and 4.91, respectively. This high level of sensitivity to interest rates, exacerbated by historically tight spreads, could be a tailwind for performance if interest rates increase.

Quality: The Local Currency Sovereign and Hard Currency Corporate indices have Investment Grade average qualities of BBB+ and BBB-, respectively. The Hard Currency Sovereign index has a High Yield average quality of BB-. It can be more difficult for countries to issue Local Currency debt or for Emerging Market companies to raise capital through debt issuance with a below Investment Grade rating, thus, the Local Currency Sovereign and Corporate indices are skewed towards Investment Grade names. Additionally, countries are more likely to default on their debt if their interest and principal payments are due in USD (as the government cannot simply print more local currency money to meet debt payments, and instead must have adequate foreign currency reserves), making downgrades in the Hard Currency Sovereign index more likely.

Liquidity: Hard Currency EMD Corporates are relatively less liquid, as reflected in higher average bid ask spreads of around 70-75 bps under normal market conditions and lower trading volumes, and thus more prone to liquidity events during broad market sell-offs – although notably they fared well during the pandemic-related downturn, as their strong fundamentals and local investor base placed them in good stead. Local Currency Sovereigns are the most liquid (bid ask spreads of around 40-45 bps), while Hard Currency Sovereigns sit in between (60-65 bps). For comparison, average US High Yield spreads are in the range of 50-75 bps, while US Investment Grade Credit has significantly lower bid-ask spreads (generally below 10 bps). Local Currency Sovereigns are more liquid than the Hard Currency sub-sectors due to the greater liquidity of currencies relative to bonds, the higher minimum issue size for the Local Currency index, and the higher quality of this index (with nearly all of the largest constituents being investment grade). Similar to most credit sectors, EMD liquidity deteriorated after the Global Financial Crisis, as broker dealers became less willing to hold positions on their balance sheets. Liquidity in EMD Sovereigns has remained relatively stable over the past decade, while EMD Corporates have seen some improvement as the sector as grown and matured.

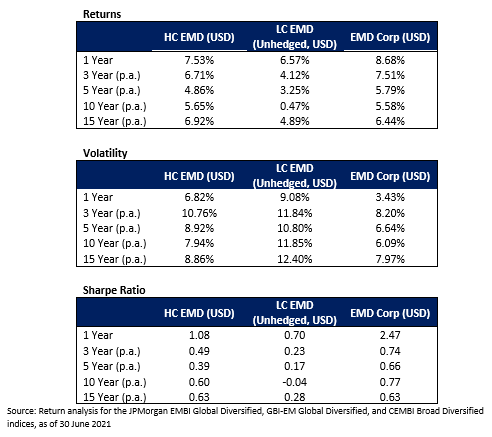

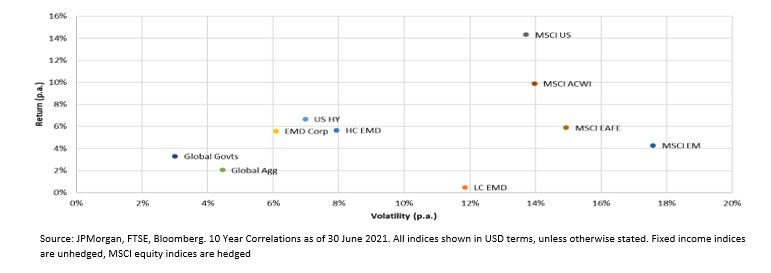

Performance

The tables below show the historical returns, volatility, Sharpe ratio, and max drawdowns for the three sub-sectors.